United Airlines posts record revenue as premium cabin demand offsets fuel hit

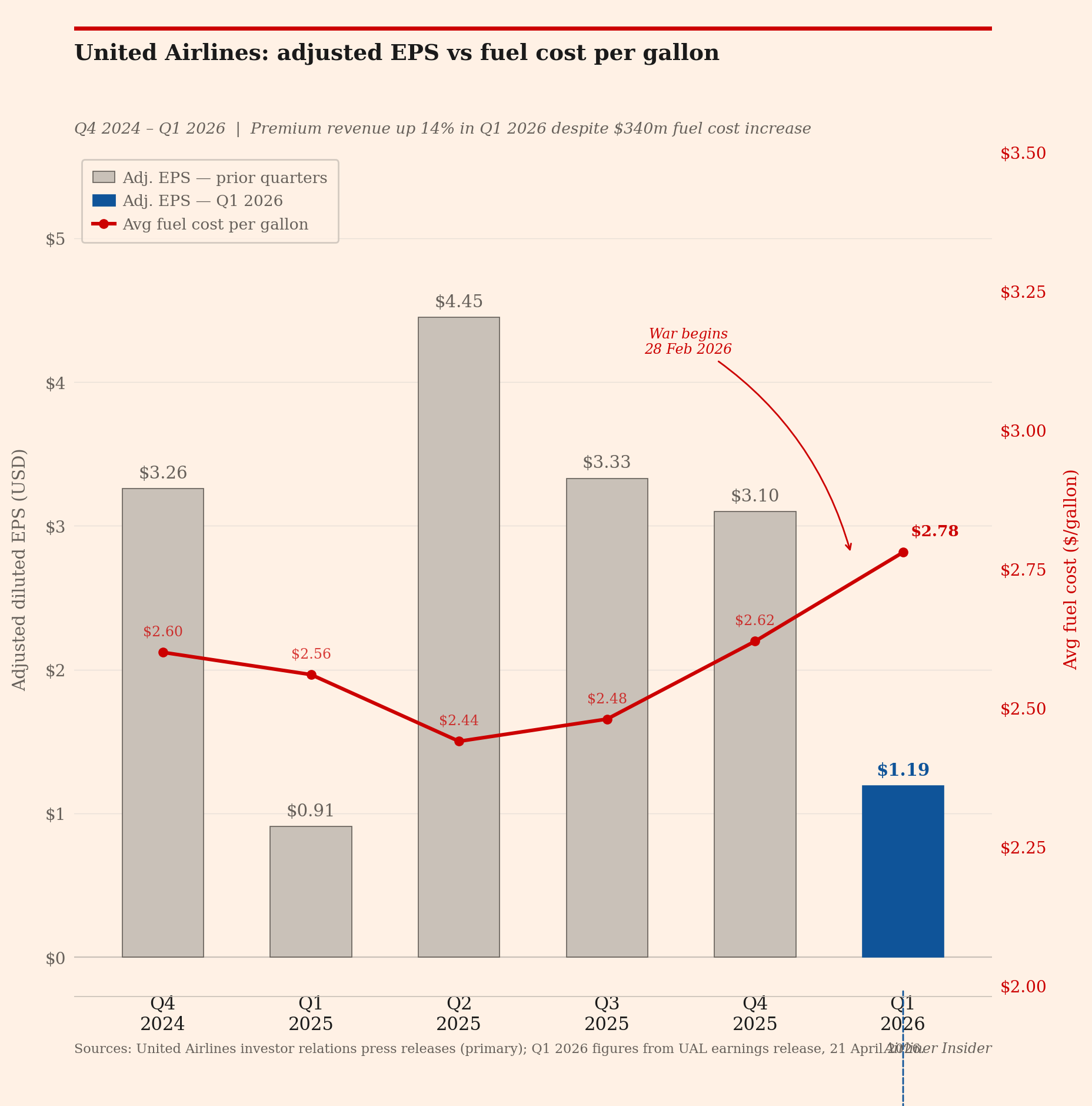

United Airlines posted a record $14.6 billion in first-quarter revenue, with adjusted EPS of $1.19 beating expectations despite a $340 million fuel hit. Premium revenue rose 14 per cent.

United Airlines reported first-quarter adjusted earnings per share of $1.19 on Tuesday, up 31 per cent year-on-year and within its guided range of $1.00 to $1.50, as record revenue and a 14 per cent rise in premium cabin sales absorbed a $340 million increase in fuel expense driven by the Iran war.

Total operating revenue reached $14.6 billion for the quarter, up 10.6 per cent year-on-year — the highest first-quarter revenue in the airline's history. Revenue per available seat mile rose 6.9 per cent across the network, with positive unit revenue growth in every region. The carrier flew more passengers in a first quarter than at any point in its history and achieved the best on-time departure rate among the eight largest US carriers for the period.

The results, reported after market close on Tuesday, demonstrate the degree to which United's decade-long push into premium revenue — loyalty, business travel and higher-margin long-haul flying — has insulated it from a commodity shock that is threatening the viability of less diversified competitors. Adjusted pre-tax margin reached 3.4 per cent, up 0.4 points year-on-year, despite fuel costs of $2.78 per gallon — a figure that reflects a quarter in which the Strait of Hormuz closed on 28 February and spot prices subsequently doubled.

The revenue thesis under pressure — and holding

The central question entering Tuesday's release was whether United's revenue diversification could absorb a fuel shock of this magnitude without margin deterioration. The answer the numbers provide is conditional rather than definitive. Premium revenue rose 14 per cent year-on-year; loyalty revenue grew 13 per cent; Basic Economy revenue was up 7 per cent; business revenue increased 14 per cent. Each of these streams performed ahead of the prior year quarter, and each contributed to a revenue base that offset the fuel increase at the operating margin line.

The more cautious read of the same numbers is that capacity rose only 3.4 per cent — United had originally planned more aggressive growth for 2026 — and that CASM-ex, the cost metric that excludes fuel, rose 5.9 per cent year-on-year. Non-fuel cost inflation at that rate, combined with an unhedged fuel position in a market where spot prices remain roughly double pre-war levels, creates a margin arithmetic that depends heavily on the revenue story continuing to hold through summer. United is already adjusting for the risk: the carrier announced a 5-point reduction in planned capacity for the remainder of 2026, with third and fourth-quarter capacity now expected to be flat to up approximately 2 per cent year-on-year, against an original plan that envisaged considerably faster growth.

CEO Scott Kirby addressed the fuel environment directly in the press release, describing the results as demonstrating the resilience of United's long-term strategy even in the face of escalating fuel expense, and noting that moments of uncertainty for the airline industry may also create opportunity for United.

Balance sheet: the less-discussed story

The financial detail that deserves more attention than the headline EPS is the balance sheet progress. United repaid $3.1 billion in debt during the quarter and, for the first time since 2019, accessed the unsecured bond market — raising $2 billion across two issuances that exceeded initial expectations. Net leverage at the end of the first quarter stood at 2.0 times, down from 2.43 times at year-end 2025. Available liquidity was $17.2 billion.

The significance of the unsecured bond issuance extends beyond the capital raised. Investment-grade credit rating access at unsecured rates signals that the market views United's credit trajectory as credible even in a period of elevated fuel costs and geopolitical disruption. Delta's ownership of the Trainer refinery provides a structural fuel cost advantage that United cannot replicate; United's answer to that asymmetry has been to build a loyalty and premium revenue base large enough to fund deleveraging through the cycle rather than depend on a single structural hedge. The $2 billion unsecured raise, executed at a moment of maximum industry uncertainty, suggests that argument is finding purchase with credit investors.

What the guidance language reveals

United did not withdraw full-year guidance in the manner Delta did on 8 April, when Delta declined to update its full-year outlook citing insufficient visibility. United's press release directs investors to the Investor Update filed simultaneously with the SEC and to the Wednesday morning earnings call for specific second-quarter and full-year targets, which means the precise guidance language will not be fully visible until the call at 9.30am CDT on Wednesday.

The capacity reduction announcement — 5 points versus the original plan, with Q3 and Q4 now expected flat to up 2 per cent — is itself a form of guidance management. It signals that United does not intend to fly unprofitable capacity at current fuel prices, which is the operationally correct response; it also implies that the full-year revenue base will be smaller than January's plan assumed, which has implications for the $12 to $14 full-year adjusted EPS range issued in January. Whether that range survives the Wednesday call in its original form is the number analysts will be focused on.

The merger question

American Airlines publicly rejected any discussion of a combination with United on 17 April, stating it was not engaged with or interested in any discussions and describing the deal as anti-competitive. Kirby's first public appearance since that rejection is Wednesday's earnings call. The press release makes no reference to consolidation or American. Analysts will press on both the rejection and whether United has identified alternative strategic paths — JetBlue has been cited in industry speculation — but Kirby is unlikely to address it substantively before the call.

The comparison that frames the results

Delta, whose Q1 results on 8 April provided the sector's first read on the fuel crisis impact, reported adjusted EPS of $0.64 and withdrew full-year guidance. United's adjusted EPS of $1.19 — nearly double Delta's — reflects the structural difference between the two carriers' fuel positions rather than superior operational execution. Delta's Trainer refinery, which provided approximately $300 million in Q2 fuel cost benefit, did not provide the same scale of advantage in Q1; United's MileagePlus loyalty programme and premium cabin revenue mix provided a revenue-side offset that Delta's refinery advantage did not need to replicate. The two carriers are solving the same problem through different structural mechanisms, and the Q1 results suggest United's mechanism — revenue diversification over commodity hedging — is working under current conditions.

The test of that mechanism arrives in Q2, when United has guided fuel at a materially higher cost than Q1's $2.78 per gallon, the summer capacity reductions will be visible in the revenue line, and the Islamabad talks will have either produced a durable Hormuz resolution or confirmed that the fuel environment remains elevated through the peak travel season.